Automated Investing - the Silent Killer of Portfolios

As investing grows in popularity—a positive trend in every respect—so does the prevalence of enabling the "automatic investing" feature in brokerage accounts. While this approach appears disciplined and hands-off, it limits portfolio growth for millions. More importantly, the risks associated with auto-investing can undermine its supposed aim: removing the guesswork from investing. Let's dive in.

A False Bull Case

Auto-investing is often praised for mitigating common investor mistakes, such as short-term market timing or abandoning investments due to volatility. While this approach certainly helps beginners avoid poor decisions, it comes at the expense of potential gains. By "avoiding" mistakes, investors relinquish active control and depend on scheduled contributions to match market dips—an impossible alignment. Strictly automated investors are often outperformed by those who reserve some capital to invest in periods of higher volatility or market downturns.

The Opportunity Cost of Easy Investing

The reality of steadily adding to investments is the sheer amount of missed opportunity. When your portfolio systematically buys during a bull market, you significantly reduce your compound growth potential. Conversely, during market downturns, savvy independent investors can hedge prior gains and deploy more capital in a market sale. The compounded effect of consistently missing these opportunities can add up to thousands, tens of thousands, or even hundreds of thousands of dollars—money that could have been yours with just a little more effort.

"It can't be that significant, right?"

wrong.

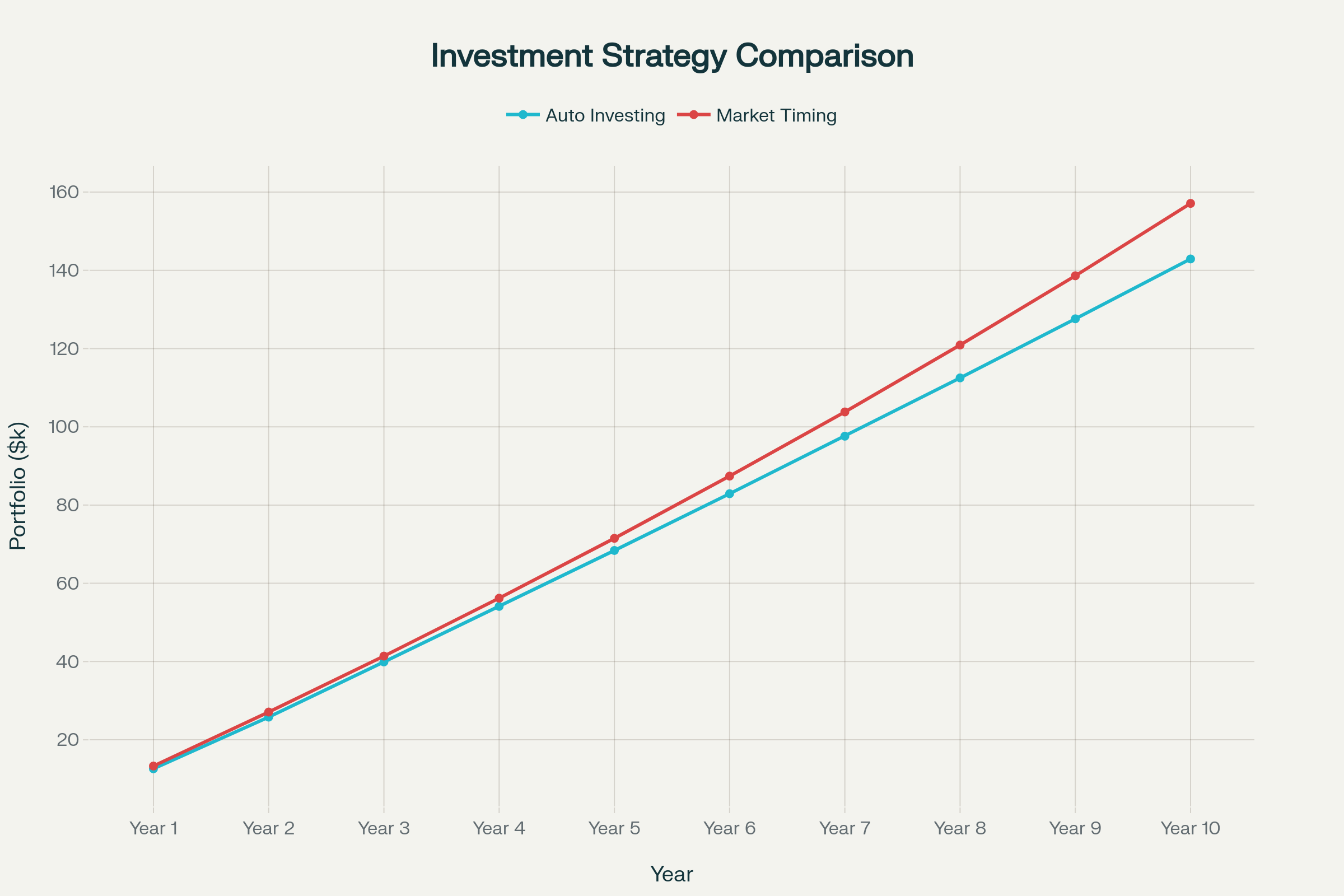

Above is a hypothetical comparison of two $10,000 portfolios over ten years: one that only buys the S&P 500 during reasonable market downswings, and another that steadily invests in the S&P 500 regardless of market conditions. While both portfolios track closely at first, the extra compounding from selective investing becomes clear, costing the steady auto-investor over $10,000. While $10,000 over a decade might not sound dramatic, let’s look at chart #2:

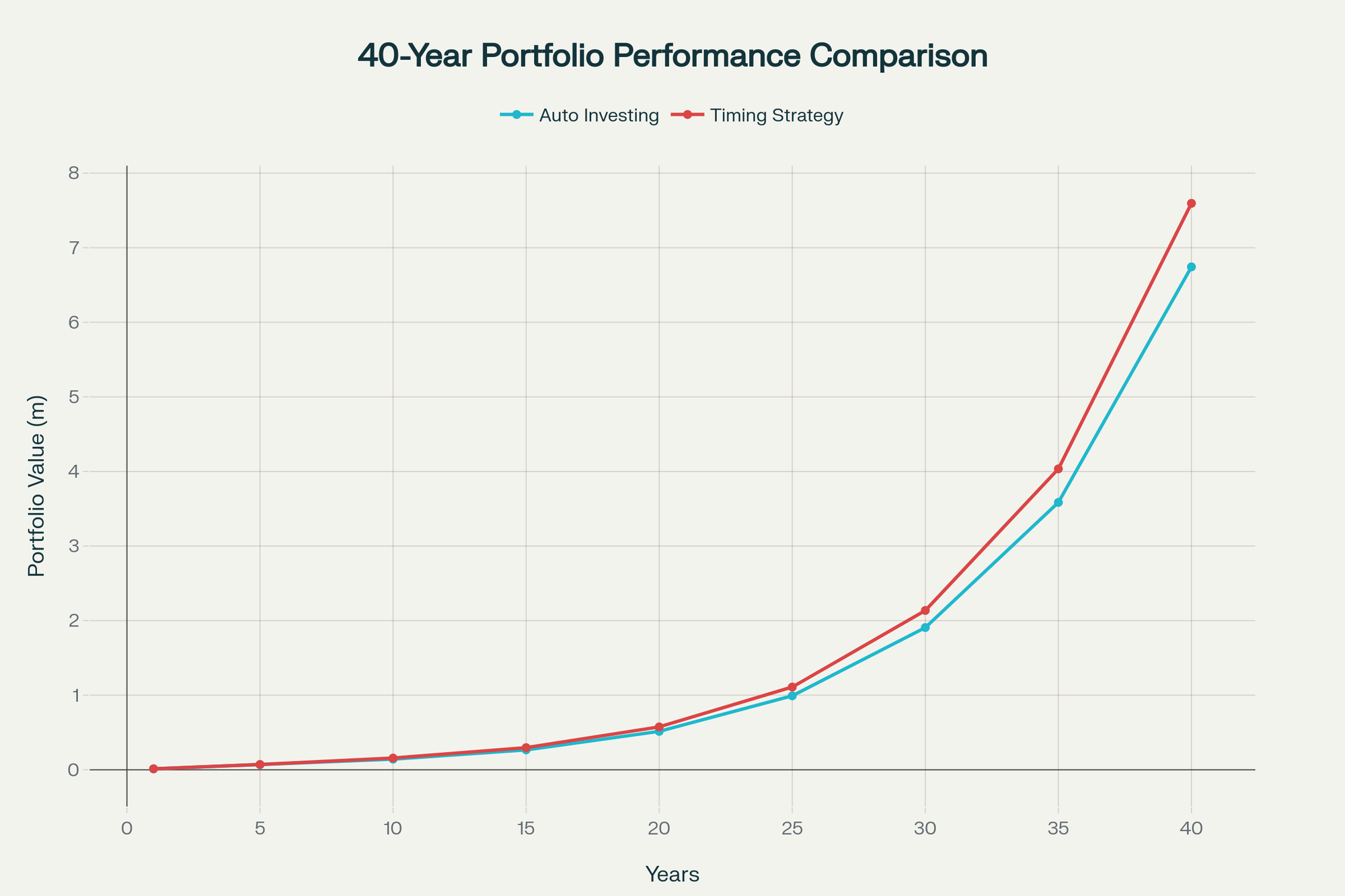

When compounding over forty years, the auto-investor is behind by a staggering $800,000. This assumes only investing during clear S&P 500 downturns—a strategy you can learn in a single Monk Investments article. That’s potentially $800,000 extra. If you enjoyed this article, subscribe to our free newsletter to receive future issues directly to your inbox. Plus, I’ll update you about the major upcoming rework to Monk Investments. You won't want to miss it.

*This article is for informational and educational purposes only. It should not be considered financial, investment, or trading advice, nor a recommendation to buy or sell any securities or financial instruments. Past performance is not indicative of future results. Markets are volatile and unpredictable; no indicator is foolproof.

Source: