Breaking Down Our Big Three - Starting Over With $10,000 | Week 4

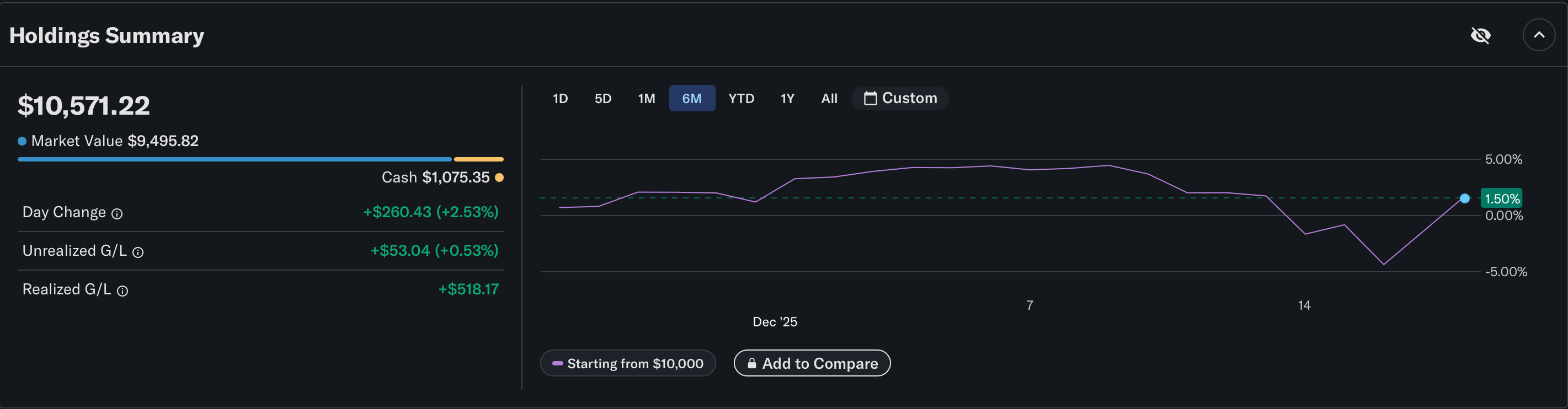

This week was a roller coaster for the portfolio. A very boring roller coaster—one sharp decline at the start of the week, and one another sharp increase at the end. Having our total portfolio value dip below our original balance of $10,000 briefly, before rising almost $200 higher than last week’s close at $10,571.17. The trades were few, but the conviction and optimism is plentiful.

Summary of Current Holdings

Our current holdings haven’t changed much besides adding a new position and seizing a DCA opportunity for an older position. Let’s breakdown a few of the heaviest allocated individual positions and the why behind them.

Amazon (AMZN)

As communicated by the portfolio, I’m extremely bullish on AMZN—holding both the 2x leverage shares and a $240 April call. The call is not looking great with around 22% in the red. However, we have 4 months left for the underlying stock to increase close to 6% to be in the money (if worse comes to worse, the -50% stop loss will close the trade). But enough about the AMZN positions, allow me to explain why I’m bullish on them.

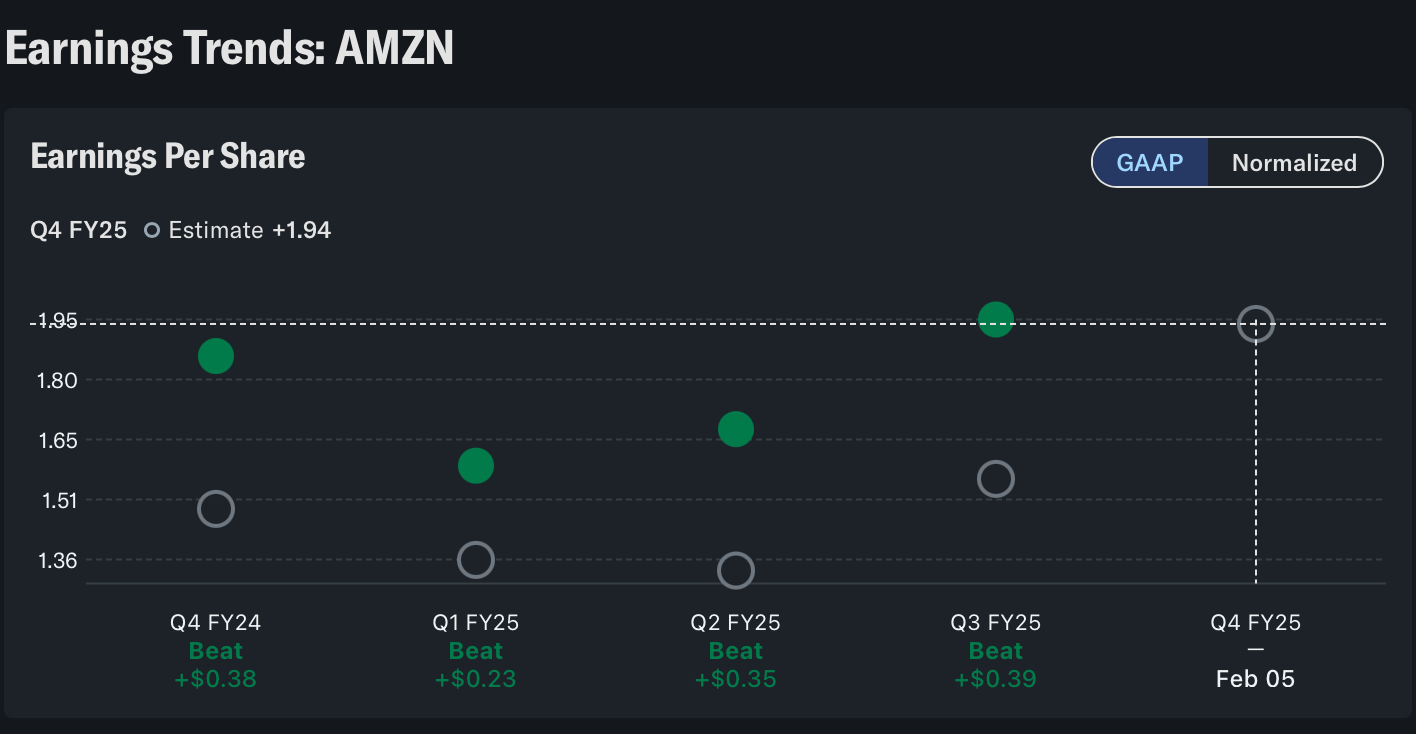

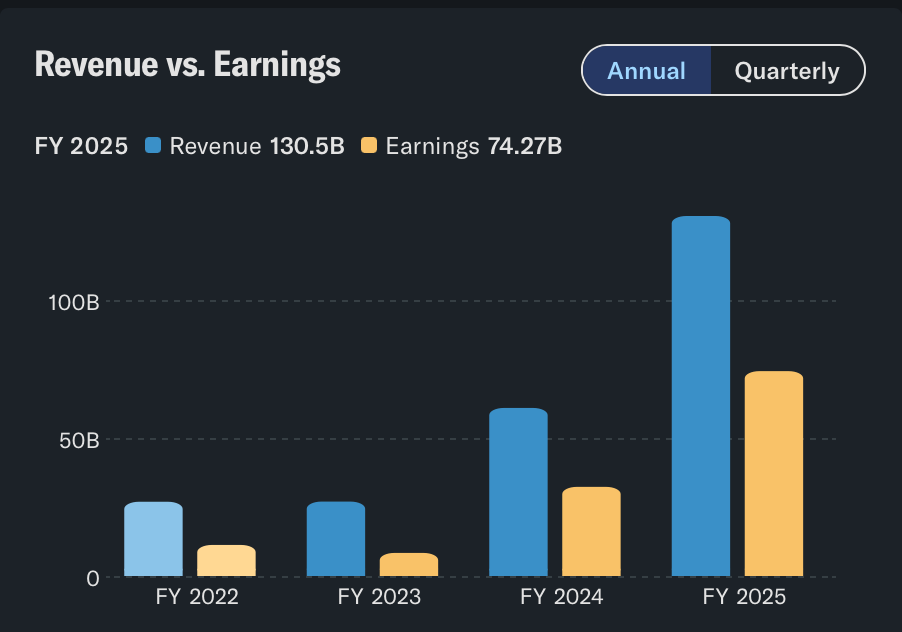

AMZN is setup to run wild in 2026. If we look at its profit printer, AWS (Amazon Web Services), the revenue rate is $130 billion annually. With margins bouncing in the low-to-mid 30s. Thus, carrying the EPS for AMZN’s shareholders, with expectations only growing because AMZN keeps beating them. Not to mention that the need for AWS is only going to continue growing with AI workloads scaling. This is why AMZN (and many other companies like it) are pouring heavy capex into new data centers and AI capacity. Many analyst agree with my conclusion with an average price target of $295.60 next year, the lowest of those being $245 of 67 different analyst. Below is AMZN’s past 4 EPS reports with their expectation in Q4, Feb 5, 2026.

Needless to say, I’m bullish on AMZN, but not for any foolish reason. Not only is this company at my doorstep every day, my favorite streaming platform, but an indispensable giant in the growth of AI.

Nvidia (NVDA)

Nvidia is one of my favorite stocks of all time. Being my biggest win in my personal and (other) experimental portfolio; and here I am writing how they are still undervalued. I purchased another $521.47 worth of 2x leverage NVDA shares when they dipped in the low $170s on 12/17. Which was near the bottom of their chart this week; THIS is why DCAing stocks you have high conviction on is important. With the leftover cash the portfolio was sitting on, I didn’t need to do research on good buys, nor on the stock I wanted to DCA. The thesis stays the same, all I needed was the stock to hit my buy price target, which was $173, for me to add to the position. Now, the shares added on that dip are up over 11%, bringing the total unrealized gain to slightly over 6%. Again, enough talk, here’s why I love Nvidia.

Nvidia’s margins are simply absurd. The gross sitting in the low 70s, majority of that owed to their AI data center and CUDA. Obviously, like AMZN, as demand for AI workload grows, the need for Nvidia’s product (chips) will only increase. Beyond the unheard of financials, NVDA’s P/E and PEG is the lowest it’s been in over a year. In addition to this, their price-to-sales and price-to-book is the second lowest it’s been in the same timeframe.

Unlike some would argue, all of this is backed by the numbers. NVDA has seen exponential growth in both revenue and earnings the past 2 years, and demand is only growing.

NVDA is an AI powerhouse, making it in today’s world a revenue and profit powerhouse. Especially with how well priced it is currently, it feels like a no brainer for this portfolio.

Netflix (NFLX)

Just like Amazon, Netflix is in close to every home in America. With all of the Warner Bros Discovery (WBD) deal-noise, NFLX has seen a hefty drop this month. Dropping around 15% from $106 to its current price of $94.39. With the uncertainty of the deal, I bought normal shares in case of a sudden drop; purchasing 13 shares at $94.39.

The deal aside, NFLX is a great buy right now; like NVDA, their PEG and P/E is the lowest it’s been in the same one-year time frame. With a bad earnings report in Q3, most investors have been wary of getting back into the stock, as it’s currently only up 4.64% this past year. As of recently, NFLX has made the infamous ‘death cross’ pattern (50 day MA and 200 day MA crossing), with the stock being $14 a share lower than the 50 day MA. The thing is, NFLX is no stranger to mighty drops; such as the one in mid 2022 that cratered them almost 75%, before rebounding 6x from the bottom to top of the chart, all within 3 years! In conclusion for NFLX, hasn’t had a terrific past 3 months, but their revenue and earnings has only grown—quarter over quarter, and year over year—so no matter the direction of the deal or where the stock goes in the short term, NFLX isn’t foreign to dramatic recovers, making me a confident shareholder.

Conclusion

I hope you enjoyed this dive into the three heaviest allocated/bullish positions in the portfolio. If you’re new to Monk Investments, consider subscribing to see more post like these. If you aren’t new to Monk Investments, consider upgrading your subscription to Pro for only $5.99/month to get more analysis like these—and track the progress of our experimental portfolio! Until then, thank you for reading, and feel free to reach out/reply to me for any questions, comments, or concerns.

*This is NOT financial advice, simply an experiment in a paper portfolio. I am not encouraging positions or trades, only education and doing your own research.

Couldn't agree more. Your AMZN thesis on AWS is totally solid. Considering how AI is accellerating, what if the generative AI boom pushes AWS demand even harder than current projections? That 'boring roller coaster' could be the calm before a very fun storm.

My portfolio was a (boring) rollercoaster this week too. Drew down to -0.4% and ended up 0.4% on the week.

The explanations of position selection were helpful. Lots of thoughts and too little time to dictate them all. Three major questions I think you could help with:

1) In your options trading, are you interested in holding these till expiration, or is this more of a short-term play with a long runway, just in case? It's unclear to me why the April strike was selected for Amazon over a LEAPS. Not sure how you're accounting for timing in this trade, and whether you're interested in holding through the tail risk of February earnings, if you intend to roll, etc.

2) When selecting between stock positions and leveraged single-stock ETFs, what is the criteria (even if it's rough) for deciding between the two instruments? I've only ever utilized leveraged positions for extremely short-term trading (1 week max) because I'm not willing to bear the black swan risk of getting wiped out x2 or x3 by holding these positions long-term, but I'm interested to hear your reasoning.

3) When selecting between stocks, what is your prioritization between fundamental and technical analysis? Do you tend to value one over the other? And does that influence your time frames for the trades? I ask because I have never considered holding leveraged positions for fundamental reasons, since I have assumed that LEFTs are short-term trading vehicles and that technicals reign supreme on short timeframes. Perhaps there is a difference in opinion about how long one should or could hold these kinds of 2-3x leveraged instruments.

Very curious to hear your thoughts. Thanks again for the time you take to reply to these. I know I don't ask easy questions.

Cheers!