Risk vs. Reward | Why Higher Returns Demand Higher Risk

In investing, there seem to be two sides of the pendulum that take turns being popular among beginner investors. These two sides, of course, are the high-risk, high-reward and low-risk, low-reward options. The tug between these two sides is called the ‘risk-return tradeoff’; the safer your investment, the lower your expected returns are, and vice versa.

The reason why this matters for beginners is that it’s easy to be swayed one way or another and close off investing or trading ideology from the other. Here is a visual of the risk-return continuum:

Here’s My Hook:

Imagine an investor puts $100,000 split into a high-yield savings account, bonds, and treasury bills. His returns are low, but he also knows himself and how he can’t handle additional risk. Another investor invests $100,000 in individual growth stocks and engages in a lot of mid-term swing trading. He’s watched his account dip down 40% twice and held all positions during this, and he couldn’t be happier with the current state of his account.

You may be thinking I’m going to ask, “Which investor has made more money?”, but my point is better proven by asking, “Which investor was able to sleep at night?” Both! Neither of these investors did the wrong thing; they both did what was comfortable for them and stuck with their strategy. Both investors could likely learn something from each other. So instead of finding a strategy that is all about the money, buying into the FOMO of a position, ground yourself, and find what works best for you.

Recommended Allocations

Below, I will list three different portfolio setups: conservative, moderate, and growth. These are general investing strategies, and you may find something to like from each one. A strategy is made to be your own if it achieves your vision. Remember, from the two investors, both could likely learn something from each other.

Conservative

60-70% in bonds, 30-40% in high dividend mutual funds

Expected annual return: ~5%

Worst year loss: -10%

Sleeps like a baby, never checks the account

Moderate

70% in individual stocks, 10-20% bonds, 0-10% cash (for buying power)

Expected annual return: ~8-9%

Worst year loss: -25%

Occasionally, fearful, manageable panic in bad markets

Growth

100% in growth stocks

Expected annual return: 12-20%

Worst year loss: -45%

Loves staring at the account all day, constantly looking for opportunities. Couldn't care less if the account is down, it’s seen as a part of the process.

3 Solid Rules for Beginners

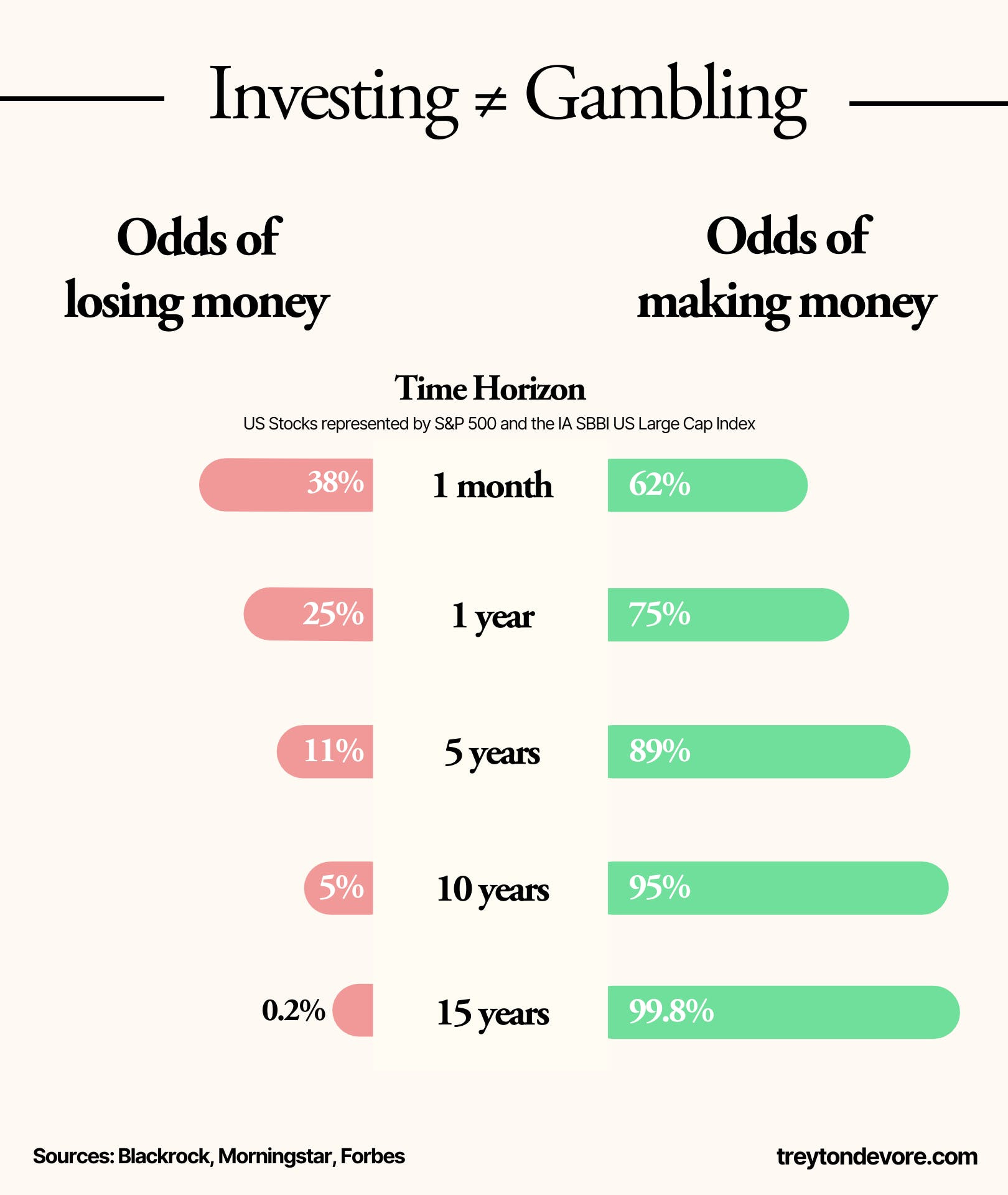

Rule 1: Your time horizon changes your gains

It’s a shame to see many new investors put their money in something for 1 month and be disappointed when it’s red. Most of the time, for these people, it’s not a bad stock that made them lose, it’s their rapid timeframe. Here’s a chart to further prove this phenomenon.

So if you’re investing with a 20+ year timeline horizon, the odds are that even with a highly aggressive portfolio, you will make money. On the other hand, if this money is needed within the next year, the odds are in your favor but less likely than what most are comfortable with, so you may want to lean more conservative with your portfolio.

Rule 2: Volatility isn’t a permanent loss

We’ve all grown used to the saying, “the stock market is volatile”, but do we even truly comprehend this with our own portfolio? Think, if a stock dropped 40% in a year, that’s frightening. But if that stock gained 60% the next year, you look like a genius for continuing to hold.

The unfortunate truth is that you have to be emotionally able to look at your money go down during that -40%, and still be confident to enjoy the 60% gain. Another reason why so many beginners don’t make money when they first start investing!

Rule 3: Diversification creates a smooth ride

Another cliche: “Don’t put all your eggs in one basket!” Now, this doesn’t mean you have to get crazy and have 80 different stocks, but it also doesn’t mean $100,000 split into three stocks will suffice. Growth isn’t often straight linear in the stock market, but I prefer it to still be a smooth ride rather than wild swings every day.

I don’t have a specific recommendation on how many holdings are enough to be diversified, as it depends on many things, such as capital, age, investing goals, etc. I encourage you to audit your portfolio and do your own research on what’s best for you!

Don’t Lie to Yourself

As I conclude, I want to assure you that there is no one right way to invest. Incrementally more gains, but sacrificing my sleep is not a worthy trade in my opinion. So map yourself on the arrow and audit your risk tolerance/investing strategy; there are strings attached to the higher-returning strategies.

Risk and reward are two sides of the same coin. Asking “Should I take more risk?” will always lead to justifying dumb decisions in the hopes of making more money. Rather, asking “how much risk can I actually handle without making a wrong decision?” The latter question is the beginning of a real investing plan, fit exactly to what you need.