Warren Buffett is Wrong

The Oracle sold his golden goose at the worst possible time -- Here's proof:

A $1 Trillion Mistake in the Making

Warren Buffett has one of—if not the—greatest investing track records in history. That being said, Berkshire Hathaway is repeating the same mistake that cost them billions before, and this time the stakes are even higher. The data says he's dead wrong.

People are on edge when looking up to Buffett for guidance; Berkshire is sitting on a record-breaking $300B+ cash pile and continues to trim positions in companies that other institutional players are buying aggressively.

One position in particular—a company Buffett already admitted he was wrong about—was quietly sold. By the time we get to the data, you'll understand why this might be the most expensive exit of his career.

The thesis of this article revolves around the recent *capital expenditure "mega-cycle" within the Magnificent 7 (the seven biggest publicly traded companies). It's one of the most misunderstood investment stories on Wall Street—and apparently, even Buffett's framework can't see it. One company in particular proves exactly why.

*[Free article where I break down what capital expenditure (CapEx) is!]

CapEx-KaBoom

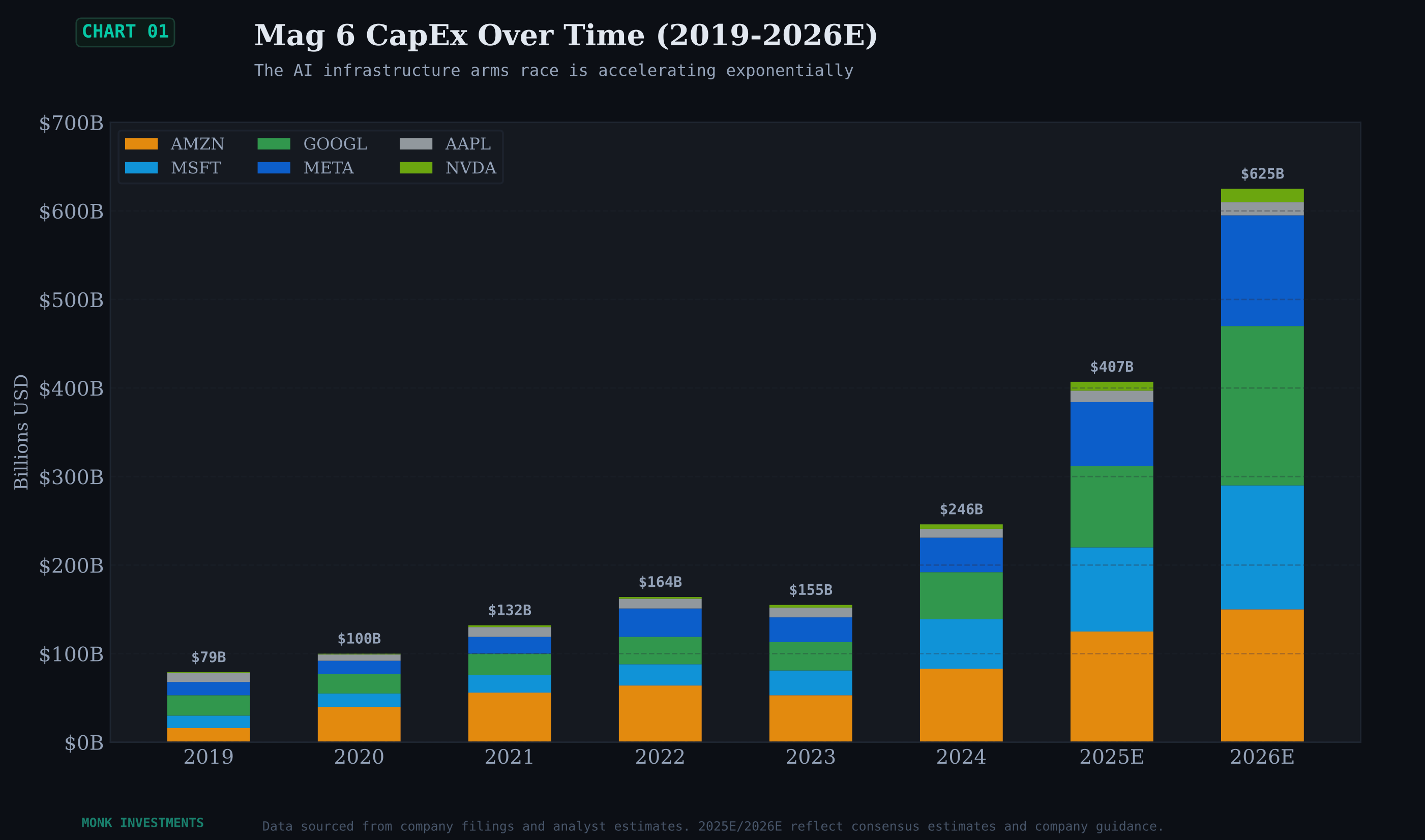

It's no secret that being in the Magnificent 7 means spending money to make money. But the scale of that spending is what has investors like Buffett concerned. The top 6 companies in the Mag 7 spent a combined $79 billion in 2019—and are expected to spend a staggering $625 billion this year.

The skeptics are asking a valid question: “Where is all of this money going?”

The answer is far simpler than you’d think. It’s not being thrown at a vague buzzword like “AI training” or some other generalized AI term. Nearly every dollar expected to be spent this year is going toward infrastructure: data centers, GPU clusters, and cloud capacity. And here’s why that matters:They’re typical investments for tech giants—just on a much larger scale.

They're typical investments for tech giants—just on a much larger scale.

The "much larger scale" isn't an all-or-nothing gamble on AI. It's keeping up with demand these companies already have for the AI models they run today.

These companies fuel each other's businesses. Nvidia supplies the GPUs for newly built data centers. Amazon Web Services provides the cloud for hosting AI models. Money flows between them in a reinforcing loop.

But one question lingers from seasoned investors: "Haven't we seen this before?"

For the Last Time, It’s Not Dot-Com 2.0

History doesn’t repeat itself, but it often rhymes.

- Mark Twain

It's easy to slap that quote onto the dot-com bubble and point it at 2026. Unheard-of spending, sky-high valuations, an unhealthy worship of AI—it's undeniably similar on the surface. But even a little research proves the comparison wrong.

Revenue and Earnings

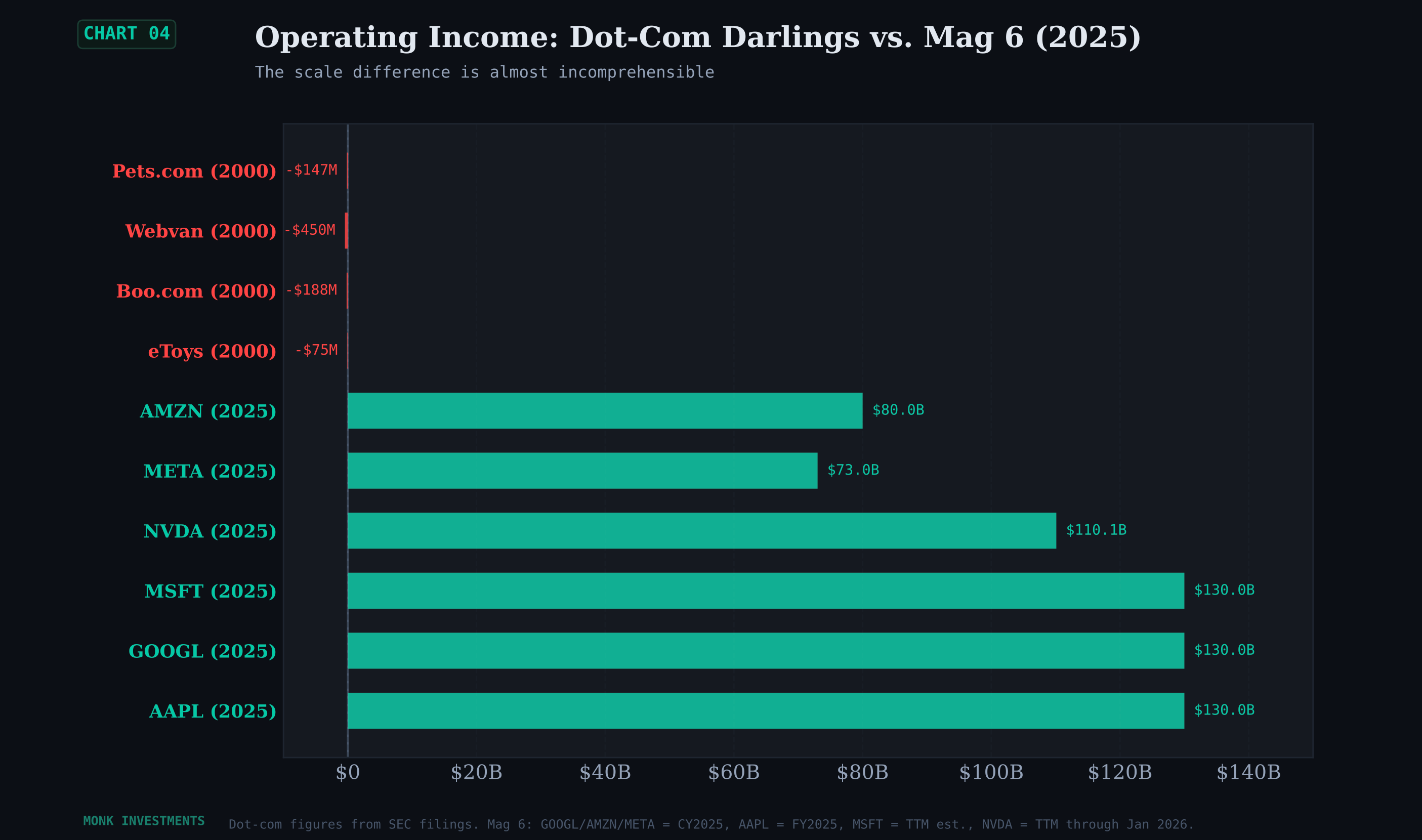

How much revenue did speculative dot-com companies generate? Essentially zero—because that's what "speculative" means. At its peak, the Nasdaq hit a P/E ratio of 200x because investors were dumping money into these companies faster than they could generate a single dollar of profit.

Compare that to today: the Nasdaq sits around a 32x P/E. The Mag 6 collectively generated ~$2.19 trillion in revenue and ~$653 billion in operating income in 2025.

Who’s Writing the Checks?

In the dot-com era, the money was smoke and mirrors—venture capital, IPO proceeds, borrowed funds. Everything except actual business profits.

Where are the Mag 6 getting their CapEx money? Not from fresh IPOs. These companies have been around for decades—and they all survived the dot-com crash. They're reaching into their own free cash flow to finance capital expenditures, backed by a track record anyone can trust. Collectively, these companies generated $200B+ in FCF in 2024 while already spending aggressively on AI.

Still, A Great Balance Sheet

Dot-com companies carried massive debt with no earnings and no assets to show for it.

The Mag 6? Roughly $350B in cash and equivalents.

So why would the greatest investor alive act like it's 1999?

Buffett’s Blind Spot — The FCF Trap

Buffett's core investment philosophy boils down to one idea: a company's intrinsic value equals the present value of its future free cash flow. It's worked brilliantly—he's found great companies with strong moats at cheap prices and held them forever.

Invert that logic: if CapEx is surging and FCF is compressing, these companies must look terrible through Buffett's lens.

And on paper, they do. But these companies don't operate based on whether Buffett considers them a good buy. They're building tomorrow's earnings, not protecting today's cash pile.

Buffett's model systematically penalizes companies in aggressive reinvestment phases. It's helped him look like a genius when the market has crashed—twice in the past four decades. Playing it safe means coming out of crashes looking smart. But investing aggressively in companies building the future? That's what separates smart from genius.

Buffett knows this, too. He has historically avoided or exited tech positions during buildout cycles, only to admit later how much he regrets it. From a 2017 shareholder meeting, speaking about a specific Mag 7 company:

I was too dumb to realize … I did not think [Certain Mag 7 CEO] could succeed on the scale he has.

- Warren Buffett

And another quote, about the same company:

Obviously, I should have bought it long ago … I admired it long ago.

- Warren Buffett

Which company? One that has proven this exact pattern before—aggressively invest, compress FCF, then watch the stock explode upward when the investment pays off. And now Berkshire is falling for the same trap again... with the same company. Selling shares they bought in 2019.

Fool me once, Buffett. Fool me once.

Allow me to reveal the biggest position in my portfolio, and Buffett’s biggest mistake: